Fad or Future: Introduction to How Cryptocurrencies Revolutionize Money & Rearchitect Trust Systems

By Manolo Sánchez

Several trillion dollars of pandemic stimuli programs across the world have reignited an interest in cryptocurrencies, which we had not seen since 2017. Fear of inflation and money printing have given Bitcoin new wings, because of its limited supply and known annual monetary supply. Some large corporations have announced plans to either hold cryptocurrency assets in treasury or accept them as a form of payment. Major financial institutions are expanding digital asset investment options to customers, and hardly a day goes by without major outlets reporting on some significant news within the crypto world. Twelve years after Bitcoin’s genesis block, mainstream investors are starting to focus on the currency and application infrastructure created by cryptocurrencies.

This recent market fascination is undeniable, but for many a fundamental question remains: why? Why should we care about cryptocurrencies, blockchain, decentralized exchanges, NFTs [non-fungible tokens], or any other new flavor of the week? Does any of this actually matter, or is it just another fad, holding mainstream attention just until we move on to the next big thing? Some public figures, over the past several years, have easily brushed off cryptocurrency as a Ponzi scheme, a tool for illicit activities, or a short-term fascination that will be irrelevant in a few years’ time.

This mindset is understandable but short-sighted. Blockchain technology enables exchange of value over the internet, reduces the need for counterparty trust, automates contractual arrangements, and beyond. No matter what segment of the economy you work and live in, these technologies will have a profound impact on how the world, as you know it, operates. Cryptocurrencies and the blockchain technology that underpins them are here to stay. Understanding the ways that this technology has already transformed our environment, and the ways that it will continue to evolve, will be critical to success in the business world of tomorrow. Annual funding of blockchain projects is in the billions of dollars and the attraction of best-in-class talent means that the space is actually moving at a faster speed. The longer one waits to come up to speed and understand this new world, the harder the learning process will be.

Bitcoin as a Breakthrough Invention, Enabled by Existing Technologies and Unique Historical Circumstances

To understand how cryptocurrency took its first steps in the world, we must look back to 2008. The global economy was in shambles, in the midst of one of the worst financial collapses of all time. Governments across the world were in the process handing out massive corporate bailouts to financial institutions, and trust in central authorities was at a low point. These circumstances and perceptions of economic inequality eventually spurred on movements like “Occupy Wall Street,” which illustrates distrust in centralized institutions. Bitcoin was born in its own unique historical context: a time when people were searching for alternatives to mainstream financial and transactional systems.

Like any other major breakthrough inventions in our civilization, for Bitcoin to be launched, there had to be a combination of mature and readily available technologies. For electronic money, the key enabling ingredients were: (a) the prevalence of P2P networks, (b) the widespread use of open-source code, (c) advanced cryptography and reliable hash functions and (d) abundant and inexpensive computing power and data storage.

In 2008, a white paper titled “Bitcoin: A Peer-to-Peer Electronic Cash System” was published by Satoshi Nakamoto (an unknown, pseudonymous individual). This paper was the first to describe blockchain technology, and it outlined in detail how Bitcoin would function. Nakamoto’s goal for Bitcoin was a system for securely facilitating financial transactions between parties without involving any central intermediary. With Bitcoin there would be no need to put trust in those large financial institutions that had failed the public during the financial crisis.

Think of Bitcoin as a form of money maintained by a co-operative of players that do not know each other, using the internet to run the shared network ledger required to keep track of the money’s credits and debits. No one can shut it down so long as a group of computers anywhere in the world can connect to the internet and run the Bitcoin software.

Because of Bitcoin, the first break-through invention, however, is our ability to uniquely own digital assets, to be able to transfer them and to do so with the certainty that there is no double spending. The transactions enabled by bitcoin-like applications are registered in permanent and immutable records for all to see. Transactions can occur rapidly, in a verifiable way, with no need for trustworthy intermediaries.

The second innovation that Bitcoin delivers is the ability to re-architect trust systems in society without the use of a central authority or third parties. In business, for instance, trust is a necessary ingredient for any economic activity. If you believe that your counterparty is unlikely to fulfill their obligations under an agreement, you will probably avoid engaging with them in the first place. Blockchain helps businesses operationalize trust in infinite new ways, particularly in the fast pace of today’s digital age. Blockchain is already being utilized to streamline business and civic practices in the world of banking, supply chain, sustainability, healthcare, voting, and much more—and development is continuing at an intense pace.

Bitcoin represented the first major steps towards a truly electronic cash system. Another cornerstone of the Bitcoin system is a limitation on supply – there will only ever be a maximum of 21 million Bitcoins in circulation, and supply is growing towards that final cap at a known rate. This design consideration was likely intended to address concern over inflation, a common fear in 2008 and today, due to the significant amount of central bank stimulus capital making its way into the economy.

For any type of money or currency to work effectively, it has traditionally needed to serve three main functions. It has needed to be a store of value, a unit of account, and a medium of exchange. Bitcoin has managed to serve some of these functions in different degrees over time. However, until there is much broader adoption it cannot function particularly well as a medium of exchange (i.e., you cannot use it to buy most goods or services). Beyond concerns over acceptance, Bitcoin’s value has long been subject to significant volatility which further undermines its use as a medium of exchange.

Programmable Money, Decentralized Applications and the Multiple Generations of Cryptocurrencies

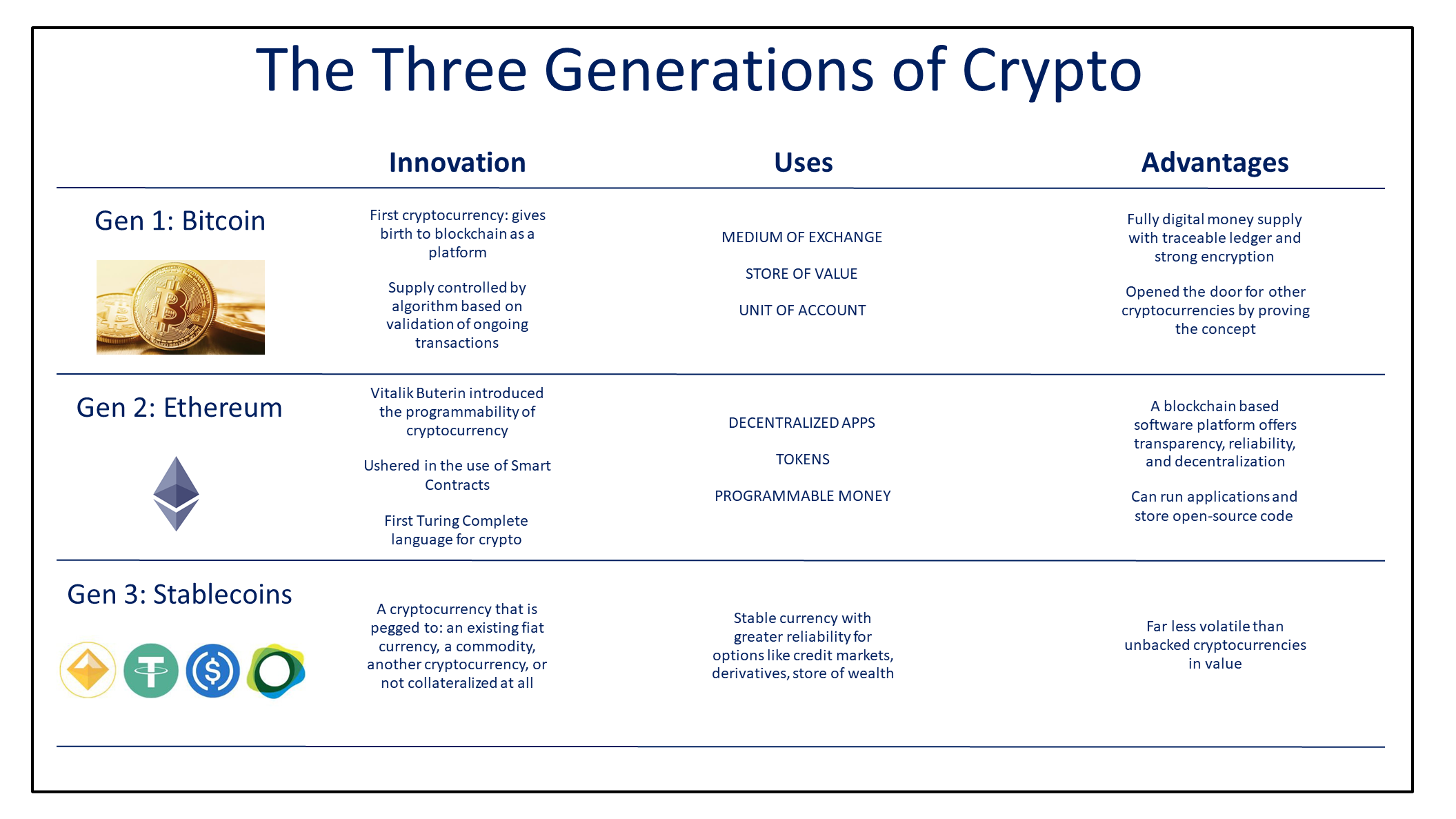

Even though cryptocurrency technology has lived a relatively short life, it has already gone through several major development cycles. We can think of Bitcoin as the flagship of a first generation of cryptocurrencies intended to facilitate exchanges of units of value: the money of the internet.

The second generation focuses on a different paradigm: programmable money. By design, and for security reasons, Bitcoin has limited programming built into it. Ethereum, is the flagship for the second generation, which adds full programmability to the formula that Bitcoin innovated. The functionality included on Ethereum makes it “Turing Complete” (given enough time, memory, and instructions, it could solve any computational problem), and lead many to refer to it as a platform instead of just a cryptocurrency. With Ethereum, users can write and automate self-executing smart contracts, issue new tokens, and run decentralized applications or organizations. There are thousands of applications currently running on Ethereum, spanning the industries of advertising, finance, gaming, art, and beyond. When used for financial and monetary purposes, Ethereum is programmable money, capable of self-executing under known conditions, any time or day of the year, without the intervention of a central authority. In fact, we can think of these platforms as infrastructure or highways for the future traffic of value on the internet.

Alongside Ethereum we have seen a fleet of competing platforms emerge. Some are full-fledged blockchains that solve or advance on the Ethereum paradigm with novel solutions. In recent times, they are known as “Layer one blockchains,” although for a while they were referred to as “Ethereum killers.” Several key cryptocurrencies that fall within this group include Cardano, Avalanche, Algorand, Polkadot, and Solana.

One growing critique of Bitcoin, Ethereum, and earlier generation cryptocurrencies is that they require a significant amount of energy to run their networks. This can result in more expensive transaction costs, public perceptions of energy waste, and limitations on scalability. While we will not delve into the technical details here, newer cryptocurrencies are switching to a system called “Proof-of-Stake” instead of “Proof-of-Work” to solve these issues. Some also intend to add interoperability between blockchains, better scaling solutions for more transactions, and various other features that will be important in unlocking other new use cases. In an ever-growing market, the “killer” name tag did not make sense for these other highways. In fact, as these platforms are adopted to run more decentralized applications, there is no zero sum necessarily.

A third generation solution has been addressing the high volatility of digital assets. The promised land of programmable money is not compatible with wild swings in value. What is the use of an economic contract that can be self-executed if the value of the conditions can oscillate 20-30% in a few hours? For that reason, we have seen the emergence of the so called “stablecoins,” which are actually tokens issued in one of the existing “layer one blockchains.” These stablecoins are pegged to a fiat currency, a commodity, assets, or basket of assets. Some are even pegged to over collateralized holdings of other cryptocurrencies. The convenience of “stablecoins” is that they deliver on operational programmable digital money. In fact, one could argue that while we await for central bank issued digital currencies, stablecoins are the digital fiat currencies of today. These stablecoins often provide a safe harbor for those trading in volatile cryptocurrency markets, and they can also facilitate an easier onramp into the world of crypto from the world of traditional finance.

Another emerging generation of crypto is referred to as privacy coins. Although Bitcoin is frequently touted as an anonymous way to transact value, the nature of its public ledger system means that a user’s identity can often be tracked down if the searcher is persistent enough. A newer batch of cryptocurrencies including Dash, Monero, and Zcash have set their sights on true transactional anonymity through a variety of technological advances. While these privacy coins are advancing the cause of a decentralized, trustless, and completely anonymous system, they do often run afoul of many regulatory regimes in the world.

Current Technological Adoption and Looking Forward

In the lifecycle of any major technological shifts, there is usually a long period of development, improvement, and consumer adoption before anything becomes a generally accepted part of everyday life. This pattern can be seen in solutions like Google’s search engine (now the backbone of global web-surfing activities) or Amazon’s ubiquitous consumer shopping platform. Cryptocurrency and blockchain markets are still very much in the process of designing and implementing the best technologies, but they are also moving quickly into the realm of mainstream adoption.

Recently the total market capitalization of cryptocurrencies reached briefly the $3 trillion mark, and there has been more than $100 billion locked into decentralized finance applications. Beyond even these public value markers, large companies like IBM, Amazon, Bank of America, and more are already utilizing some permutation of blockchain technology in their daily business activities. This adoption is far too significant to ignore and demonstrates that cryptocurrency and blockchain technologies are rapidly becoming an integral part of the global economy.

Many believe that we are currently in the investment phase of blockchain and crypto system development. As widespread adoption continues to grow and more value makes its way into the blockchain and crypto ecosystem, more businesses and individuals will be able to gain utility from these systems. Eventually we expect the market, that has been characterized by speculation and wild volatility, to transform into a more stable framework of infrastructure that the new global economy will be based on.

Epilogue for the Shipping Industry

What if blockchain technology could solve problems in industries where players should not or prefer not to trust each other? What if blockchain technology could synthesize the stacks of paperwork that some industries still use while maintaining an incorruptible and immutable record of every step of the process?

Through a joint venture, Maersk and IBM became one of the first players in this space, applying blockchain technology to solve supply chain inefficiencies and trust problems. Global trade is executed using vast amounts of documentation and little transparency. When the process is analyzed, it could seem that the technology dates back to the pre-container era. The industry does not only rely on a large number of players, but on physical documents, papers, and stamps which are error-prone manual processes.

The joint venture’s creation to solve these problems with blockchain technology was named TradeLens. TradeLens is a blockchain-based platform which is made available to every stakeholder in the shipping ecosystem including freight forwarders, ports, shippers, custom authorities, and shipping lines. This digitization of the supply chain contains all the major data and information needed to track and trace a shipment. Stakeholders in the platform are also able to submit, validate, and approve documents across organizational boundaries. Similar to Bitcoin and other cryptocurrencies, one of the biggest challenges is adoption. If the whole ecosystem does not adopt the technological platform, the value proposition loses relevance. In contrast to Bitcoin, TradeLens uses a permissioned configuration, where certain stakeholders have access only to the information that they need for security and privacy purposes. For example, competing carriers are not able to access each other’s pricing and forwarders do not have access to each other’s cargo information.

There are several other benefits that this technology will bring about in the industry, including cutting the cost of maritime fraud. Blockchain’s operational benefits, could eliminate the physical documentation portion of the process, which is estimated to be as high as 20% of the overall cost of the physical transportation. It is clear that even though adoption of a technology in an industry of this size is a very difficult task, it is an effort that will pay for years to come.

About the Author

Manolo Sánchez is a director at Fannie Mae, Stewart Information Systems and BanCoppel (Mexico) after having served as chairman and CEO of BBVA Compass for 10 years. As an adjunct professor at Rice University’s Jones Graduate School of Business, he teaches disruption in financial services with a focus on cryptocurrencies and blockchain.