Moving the Needle on Cargo Emissions

Navigating difficult waters is nothing new for the maritime industry. From the implementation of double hull tankers and ballast water systems to more recent challenges of continuing to operate during a pandemic, the marine industry has a rich history of overcoming big challenges.

Navigating difficult waters is nothing new for the maritime industry. From the implementation of double hull tankers and ballast water systems to more recent challenges of continuing to operate during a pandemic, the marine industry has a rich history of overcoming big challenges.

By Lance Nunez, The Dow Chemical Company

We have seen the issue of marine emissions on the horizon for some time now, but each day, it becomes more evident that emissions (and the need to reduce those emissions) will have a tsunami-like impact on the marine industry. Rising to this challenge is essential to the viability and sustainability of our industry and our world. Climate change widespread, rapid, and intensifying – IPCC — IPCC.

From a broad perspective, the Paris Agreement of 2015 represented the biggest global consensus on the need to reduce emissions to date. In the Paris Agreement, 196 parties entered into a legally binding international treaty to limit global warming to well below 2 degrees, preferably to 1.5 degrees Celsius, compared to pre-industrial levels.

Given the international nature of the marine industry, the task of regulating maritime emissions was intentionally left out of the Paris Agreement and passed to the International Maritime Organization (IMO). The Fourth IMO GHG Study 2020 estimated that total shipping emitted 1,056 million tons of CO2 in 2018, accounting for about 2.89% of total global CO2 emissions. In effect, maritime emissions were just short of Japan’s emissions (fifth largest emitter of CO2). (Fourth Greenhouse Gas Study 2020.)

With the rest of the world reducing emissions and global trade continuing to grow, failing to address maritime emissions in a meaningful way would result in maritime emissions becoming an ever more significant part of global emissions. From both the perspectives of the planet and the industry, this would not be a sustainable situation.

To cover the various rulemaking actions being taken and considered by IMO is beyond the scope of this article (Air Pollution, Energy Efficiency and Greenhouse Gas Emissions (imo.org)). Suffice it to say that some regulations are already here and plenty more are coming as IMO aims to achieve total annual GHG emissions reduction by at least 50% by 2050 compared to a 2008 baseline.

IMO is not the only regulatory body setting targets and planning regulations. For example, the European Commission recently announced that it intends to move forward with including maritime emissions in their Green Deal legislation. Their “Fit for 55” plan would introduce measures aimed at reducing maritime emissions 55% by 2030 within the EU and on international voyages arriving or departing from Europe. Europe is looking to lead the world by being the first major trading bloc to be carbon neutral by 2050 (Climate action and the Green Deal | European Commission).

Beyond the regulators, there are many efforts and initiatives underway demonstrating foundational support for emission reduction and a bias for action. Companies such as Ford, American Airlines, CEMEX, Verizon, Total, BP, Dow, Shell, Stolt-Nielsen, Maersk, Odfjell and have made public net zero/climate neutral 2050 commitments. They join an ever-growing number of individual companies are making their own reduction plans, setting their own emissions reductions targets, and taking real action. Some, like IKEA and Microsoft are committing to carbon negative targets.

Speaking from the perspective of Dow, emission reductions are in line with our mission to create solutions for the world’s toughest challenges. The need to reduce emissions is a clear message we receive from scientific evidence as well as from investors, customers, society, and our own employees who increasingly want to invest in greener companies purchase greener products, and perform their work more sustainably.

With the growing number of companies making carbon reduction commitments, there is a growing need to find suppliers and carriers who share the same vision and bias for action. No company can get to net zero emissions in a vacuum, and many are finding it advantageous to work together with suppliers, carriers, other like-minded companies, and industry associations to set targets, leverage best practices, and drive action.

An example of companies coming together for the sake of emissions reductions is Sea Cargo Charter. Sea Cargo Charter was founded in 2020 by seventeen inaugural signatories for the purposes of establishing a framework for assessing and disclosing climate alignment of chartering activities related to cargos shipped in bulk vessels (solid, liquid and gas). Since its launch, the number of signatories has grown to twenty-four.

While the technical guidance for how Sea Cargo Charter gathers and calculates emissions was created to specifically address the bulk marine transportation industry, much of its governance structure was inspired by and aligned with the Poseidon Principles. (Another example of a key industry partnership to reduce emissions, the Poseidon Principles was launched in 2018 and was crafted to establish a framework for assessing and disclosing the climate alignment of ship finance portfolios).

From an operational perspective, Sea Cargo Charter signatories establish contractual reporting agreements with their respective carriers. Per these reporting agreements, carriers use standardized data templates to report emissions aligned to the respective charterer after each voyage.

Annually, charterers report their aggregated emissions versus climate alignment trajectories. Climate alignment trajectory targets are calculated from the latest available climate studies and lay out sequentially tighter annual targets that track towards achieving 50% emissions reductions by 2050. The data gathered from carriers provides a basis for understanding and reducing emissions while the annual reporting helps to keep charterers accountable for ever increasing reductions. The increased transparency and accountability improves decision making at a strategic level and shapes a better future for the shipping industry and our society.

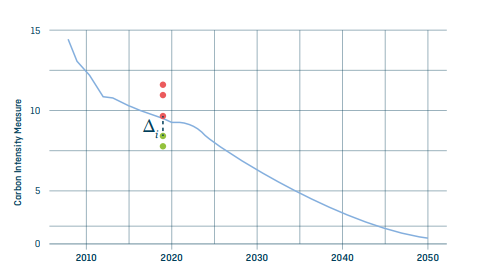

In Figure 1, each dot represents the carbon intensity of a charterer’s emissions and the blue curve represents the decarbonization trajectory for a given ship type and size (i.e. vessel category). A decarbonization trajectory is a representation of how many grams of CO2 can be emitted to move one ton of goods one nautical mile over a time horizon to be in line with the IMO’s Initial Strategy. In the figure, the green dots are aligned with the carbon trajectory, and the red dots are misaligned. The initial Sea Cargo Charter trajectories align with IMO’s target of a least 50% reduction by 2050 based on 2008 emissions. If anything, the pace and pressure to reduce emissions is growing, and as Sea Cargo Charter matures, it will continue to assess and adjust its ambitions and targets accordingly.

Sea Cargo Charter’s IMO alignment extends to the data collection design. Three standard data templates were created to facilitate carrier emissions reporting. These templates were designed collaboratively between industry associations, signatories, and carriers to accommodate bulk marine transportation sectors. This collaborative approach combined with alignment to IMO data points and calculation methodologies reduces the reporting burden and helps ensure the reporting process is sustainable.

In short, industry efforts such as Sea Cargo Charter, Poseidon Principles, Blue Sky Maritime Coalition, Getting to Zero Coalition, etc. are establishing sustainable operating paradigms, pooling expertise, and driving efforts that can jump start emissions reductions and pooling expertise, and driving efforts that can jump start emissions reductions and inform more effective rulemaking.

In whatever form, be that via company targets, industry initiatives, and/or new rulemaking, the need to reduce emissions will have a profound impact on the marine industry for the next several decades. The solutions needed range from innovations in vessel/propulsion technologies, fuel/distribution technologies, chartering agreements, and supply chain designs. Our best chance for success lies in setting aggressive targets, collaborating closely to find the best solutions, and taking effective actions. Working together as an industry, we can move the needle towards a cleaner and more sustainable future.

Lance Nunea

Lance Nunea

The Dow Chemical Company

www.dow.com